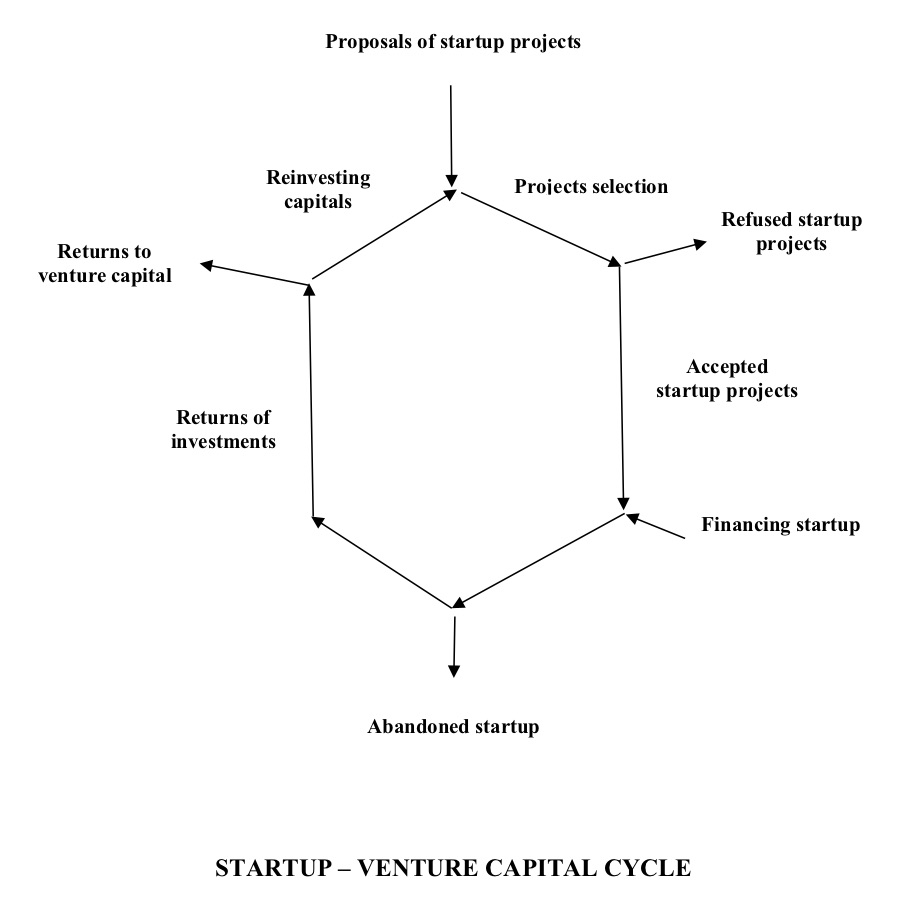

The startups financed by venture capital (SVC) are active since many years in industrialized countries and now they are of interest also in Italy. However, they have not been the object of many studies about their technological and financial processes. The Frascati manual, used as OECD guide for statistical studies, does not take in consideration the SVC system, and it is then absent in statistical studies on research and innovation.About the SVC system it has been recently published on the website of IRCrES – CNR, a Research Institute on Sustainable Economic Growth, a working paper in which the SVC system is compared with that of R&D projects. This study underlines the differences between startups and R&D projects for the presence in startups, not only R&D, but also elaboration of business models suitable for the developed technology, without limitations existing in industrially financed R&D projects by strategies of the firms financing the projects. The study, contrary to a diffused opinion, underlines that the driving force of the system lies in the radicality of the financial strategies of VC with respect to industrial capitals, as it is not interested in exploiting but in selling the developed technology and refinancing further startups.

The study develops a simple mathematical model of the SVC cycle that shows that: if the returns of investments (ROI) are high enough, there is an autocatalytic development of financing and then of technologies developed by startups. The study then considers two types of strategies: the first, typically American, that selects startups on the basis of their potential ROI and validity of the startup team, the second one, typically European, selects startups on the base of the probability of success, furthermore, differently from the first one, considers negatively the failure of a first startup attempt, hindering in this way the accumulation of experience useful for teams that attempt further startups. The American strategy is characterized by a rate of failure that reaches 90% of financed startups, while in the case of the European strategy the rate is around 70-80%. In spite of this fact the American strategy is more efficient because of the high attainable ROI from successful startups. That may be attributed to a knowhow that VC has accumulated during the years of selection and support to the financed startups. A lesson that may be drawn by this study concerns possible policy of public financing of startups in order to compensate the scarcity of private VC. An intervention of this type could be inefficient because of inexperience of public officials in selection, coaching and monitoring of startups activity in order to increase the probability of success and ROI. A public intervention may anyway be useful as seed capital for helping startups in the initial search of financing.